The Rise to Stay Short

Central Banks around the world have been working tirelessly over the past 10 years lifting the economy into some kind of growth. During this time, we saw Central Banks deeply cut interest rates to levels never seen before in our history.

They say there is a reason why they make the rear view mirror of a vehicle smaller than the front windshield – you always want to keep looking forward and once in a while look back. Keeping in mind what has happened over the past several years to the fixed income markets (also equity markets as well), you need to be positioned for a rising interest rate environment.

Over the past couple of years, we have been asked the question – when do you think Canada will raise its interest rates? This question became more and more frequent especially after the US Fed started raising their interest rates in late 2015. After the Commodities Super Cycle ended in 2015, the Bank of Canada responded with 2 interest rate cuts to help alleviate any economic impact to Canadian oil producers and to the Canadian market. However, these interest rate cuts deeply depressed fixed income yields on the short end of the curve, forcing many to invest into longer dated bonds and GICs.

Rising Rates – Not By When But By How Much!

Since May 2017, the 5 Year Canadian Treasury yield has spiked up 90 basis points, trading over 1.80% with the 2 Year Canadian Treasury trailing right behind at around 1.60%.

5 Year Canadian Treasury Yield vs 2 Year Canadian Treasury Yield

After growth expectations were reduced from lower commodity prices and further reduced after Trump threatened to tear down NFTA, we have seen surprise growth in the first quarters in Canada. GDP grew by 3.7% in Q1 and 4.5% in Q2 and job growth has been steadily increasing through 2017. With stronger than expected economic data, the Bank of Canada views that growth in Canada is becoming “more broadly-based and self-sustaining” (statement by the Bank of Canada, September 2017). So the Bank of Canada raised the interest rate twice in less than 2 months. The September rate hike took many by surprise as the markets only expected a 50% chance of a rate hike at the September meeting. The two interest rate hikes so far this year are an unwind of the two interest rate cuts in 2015; however, there is momentum for a third interest rate hike this year. Bank of Canada Governor Poloz stated the bank would remain cautious. This is on the assumption that the BoC would use two rate hikes to normalize cuts made in 2015 and the Fed would lift 3 times in total in 2017. The current implied probability for a BoC rate hike by year end is now at 59.4% while Fed chances have moved up to 70.0%. However, we have lots of time before 2017 comes to a close; our focus will be on economic data and geo-politics.

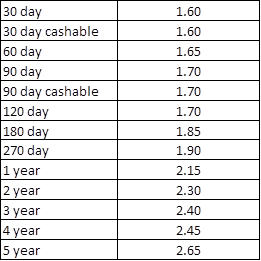

With the rapid rise in interest rates, bond yields (as indicated above) have also rapidly spiked. As Corporations manage their interest rate exposure and maximize their yields, we suggest investing in short term vehicles. Over the past couple of weeks, we have seen substantial increases in short term GIC rates. Below is an illustration showing Canadian GIC rates from various financial institutions:

For example, the 30 day cashable GIC gives you a very attractive rate of 1.60% and offers flexibility and liquidity (after 30 days). As you begin to forecast your cash flows, you can see the benefits of staying on the short end of the curve. Since we are in a rising interest rate environment, giving up 30 basis points to invest into a 6 month GIC may make more sense than locking into a 1 year GIC. As both the BoC and Fed have more of a hawish tone on raising the interest rates, we will continue to see short term rates move up, thereby making it more attractive to invest in the short term than lock into long term GICs.

For a consultation on how we can maximize your cash yields, please give us a call at (416) 777-7090.

Author:

Michael Dehal, MBA, CPA, CMA, CIM

Vice President & Portfolio Manager